The Catalyst for Change: Business Management and Collaboration

Many industries wrestle with collaboration within the face of the sustainability transition. In extremely aggressive environments, information-sharing and joint investments typically take a backseat to sustaining a aggressive edge. Nonetheless, the insurance coverage sector operates otherwise. Whereas competitors stays a driving drive, insurers incessantly collaborate by sharing massive dangers or spreading publicity via reinsurance. Brokers, too, play a vital position in balancing competitors and collaboration to safe one of the best outcomes for purchasers.

On the coronary heart of this trade sits Lloyd’s of London, a self-regulating market that has facilitated insurance coverage innovation for hundreds of years. Lloyd’s supplies a singular ecosystem the place insurers and brokers function beneath a standard regulatory framework, making certain easy collaboration and competitors. The central fund ensures payouts on legitimate Lloyd’s insurance policies, even when an insurer turns into bancrupt, providing confidence to policyholders. Moreover, Lloyd’s world licenses allow insurers to function throughout lots of of markets worldwide.

An Innovation Legacy

Lloyd’s dominance started with its unparalleled entry to delivery intelligence, making it the go-to market for maritime threat change. Over time, it has pioneered insurance coverage for rising applied sciences, launching the primary insurance policies for motor autos, aviation, and house satellites. Whereas not each innovation succeeded (e.g., airship insurance coverage), Lloyd’s has cemented its status because the premier market for insuring advanced and distinctive dangers—from Bruce Springsteen’s voice to Betty Grable’s legs.

Past underwriting, Lloyd’s has performed a proactive position in trade analysis and disaster response. The Lloyd’s Tercentenary Analysis Basis funds research into threat administration, and {the marketplace} has traditionally acted decisively in turbulent instances. As an example, after the 1906 San Francisco earthquake, Lloyd’s facilitated rapid full-limit payouts. Following the 1980’s asbestos disaster, it led structural reforms to stabilize the market.

Now, because the world faces local weather change—arguably the biggest evolving threat—Lloyd’s has a possibility to drive industrywide collaboration in assist of cleantech options.

Lloyd’s has already taken steps on this course. In 2021, it launched the Sustainable Merchandise and Companies Showcase, highlighting revolutionary insurance coverage options from trade leaders. Its Lloyd’s Lab accelerator program has nurtured insurtech start-ups similar to Kita (carbon offset insurance coverage) and AstroTeq.ai (earthquake forecasting expertise). These initiatives display Lloyd’s capacity to foster innovation, but targeted engagement with the cleantech trade stays restricted.

A Name for Extra Targeted Motion on Cleantech

Whereas Lloyd’s stays impartial relating to divestment from fossil fuels, it might do extra to leverage its market place in favor of cleantech. At the moment, non-profit initiatives like InnSure within the U.S. are main the way in which. InnSure’s local weather initiative platform acknowledges insurance coverage as a vital enabler of unpolluted power deployment. In January, InnSure partnered with Energetic Capital, kWh Analytics, and the Coalition for Inexperienced Capital (CGC) to launch GreenieRe, an impact-focused reinsurance firm designed to take away monetary boundaries for clear power tasks. With an preliminary $200M funding from CGC, the initiative goals to unlock over $30B in private-sector financing for renewable power.

Lloyd’s is uniquely positioned to take related daring motion with the contacts, authority, and deep pockets to bridge info gaps in cleantech and facilitate revolutionary partnerships to unlock scaring cleantech. At a time when its relevance to a modernizing insurance coverage market is beneath scrutiny, it has a uncommon likelihood to steer, set up, and innovate at an industrywide scale. By championing cleantech funding and insurance coverage options, Lloyd’s cannot solely assist mitigate climate-related dangers but additionally safe its personal long-term position within the evolving insurance coverage panorama

Parametric Insurance coverage: New Danger Switch Options to Deal with Risking Bodily Local weather Dangers

Based on AON, In Q1 – Q3 final 12 months (2024), the insurance coverage safety hole was estimated to be 60% ($258B of financial losses vs. $102B of insured losses) and is rising, leaving communities, companies, and people with out a monetary backstop for local weather dangers. The LA wildfires this 12 months are estimated to trigger as a lot as $250B in financial harm and account for 4% of California’s GDP.

These rising excessive climate occasions are lowering the monetary resilience of communities – after every loss, insurance coverage premiums improve for communities in Cat-loss-prone areas, resulting in extra individuals being priced out of shopping for insurance coverage. A damaging suggestions loop is created the place the insurance coverage hole then widens after every occasion, pushing the price of harm onto taxpayers, downgrading the entire communities’ credit score, devaluing properties and communities. One such resolution to bridge the safety hole is tech-enabled parametric insurance coverage.

Parametric Insurance coverage: Slightly than estimates by way of retrospective knowledge and payouts primarily based on loss, parametric insurance coverage makes projective estimates of threat by way of superior local weather knowledge fashions. These are getting used to hyper-localize threat profiles for particular insurance coverage strains (property) and perils (flood) and payout primarily based on triggers.

Triggers will be verified by direct sensing (e.g., water sensor for flooding severity) and might allow quick suggestions of occasion severity to exchange sending loss adjusters and might allow quick payouts – nevertheless, because the sensor is within the shopper’s possession, reinsurers have raised fraud issues. Instantaneous payouts ought to cut back the general value of claims for insurers, saving on pricey administrative loss-adjusting, and allow better resilience for the insured.

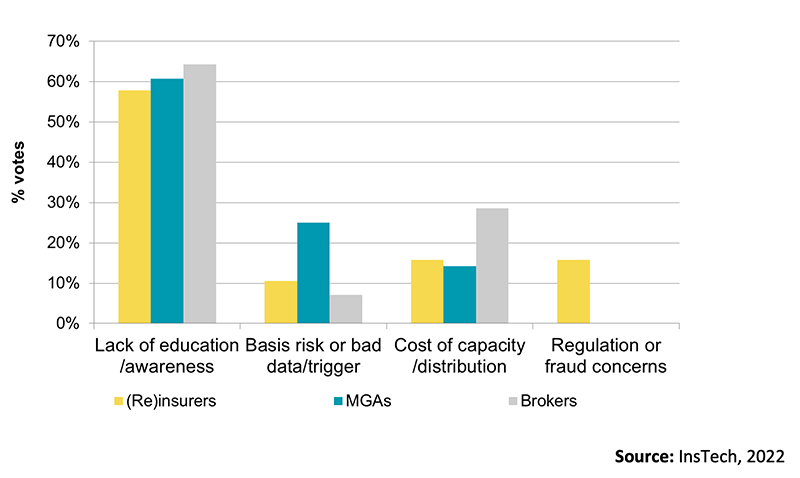

InsTech Ballot: Ballot of Insurance coverage Professionals on What’s Holding Parametric Insurance coverage Again

Amongst different innovators, Cleantech Group spoke to Tanguy Touffut, CEO and co-founder Descartes, a frontrunner in parametric insurance coverage options. When talking on the way forward for parametric insurance coverage, Touffat stated, “With the assist of our companions, we are going to proceed to develop and deploy a brand new technology of insurance coverage merchandise which might be solely tech-driven, easier, extra clear and faster to pay within the occasion of a loss – tailored for the brand new dangers firms and governments more and more face.”

In talking on the disruptive way forward for parametric insurance coverage Touffat stated, “Parametric insurance coverage can each exchange or complement conventional insurance coverage; that being stated, we anticipate to see extra covers combining parametric insurance coverage for pace and transparency for Cat perils with conventional insurance coverage for non-Cat perils.”

What’s Holding Parametric Options Again?

Lack of Information. Within the case of parametric insurance coverage, the insurance coverage insider polled dozens of insurance coverage specialists in 2022 discovering lack of training and consciousness as the best barrier (52%) as to why extra insurers hadn’t taken up parametric insurance coverage. That is particularly the case for retail brokers who’re on-the-ground promoting these merchandise. Cleantech Group spoke to parametric insurance coverage innovators, with most figuring out brokers as key gross sales channels they wanted to determine. Conversely, brokers needs to be extra proactive in exploring these alternatives in cleantech.

Tech Hole. A more moderen ballot of insurance coverage professionals on the obstacles to parametric insurance coverage in August 2024 by Reinsurance Information discovered that lack of knowledge and fashions was the best impediment to world adoption. This presents challenges the place there could also be misalignment between the pre-agreed parameters for the payout and the precise losses, necessitating using loss adjusters and delaying payouts in spite of everything.

Nonetheless, many superior and projective fashions do exist, accounting for advanced, compounding dangers of local weather change, e.g., Descartes, Sust World or Jupiter Intelligence. These options are additionally getting smarter, with proprietary and regionally-focused fashions, AI, and better entry to extra correct satellite tv for pc knowledge. Insurers have to discover partnerships with these innovators to advance and customise their fashions or outsource underwriting capabilities.

A Word of Warning

Capitalizing on rising markets in cleantech, insurers are working with innovators in earlier levels and in additional various sectors which may fast-track scaling. Nonetheless, insurers can wield important energy in shaping these markets – so they have to put money into inner and exterior experience to appropriately assist, mitigate dangers, keep away from red-tape, and finally scale cleantech.