Assist CleanTechnica’s work via a Substack subscription or on Stripe.

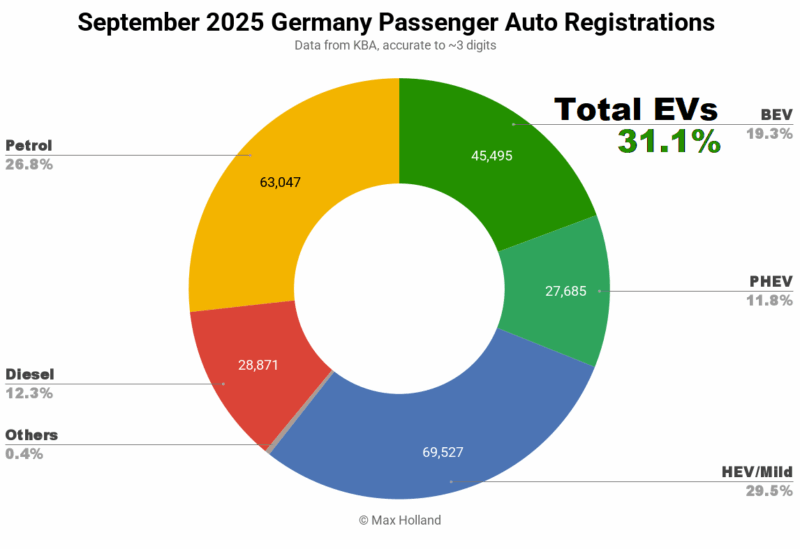

September noticed plugin EVs at 31.1% share in Germany, up from 23.7% share year-on-year. BEV quantity elevated by 32% YoY, whereas PHEVs grew 85%. Total auto quantity was 235,528 items, up some 13% YoY. September’s best-selling BEV was the Volkswagen ID.3.

September’s auto gross sales noticed mixed EVs at 31.1% share in Germany, with full electrics (BEVs) at 19.3% share, and plugin hybrids (PHEVs) at 11.8%. These evaluate with YoY figures of 23.7% mixed, 16.5% BEV, and seven.2% PHEV.

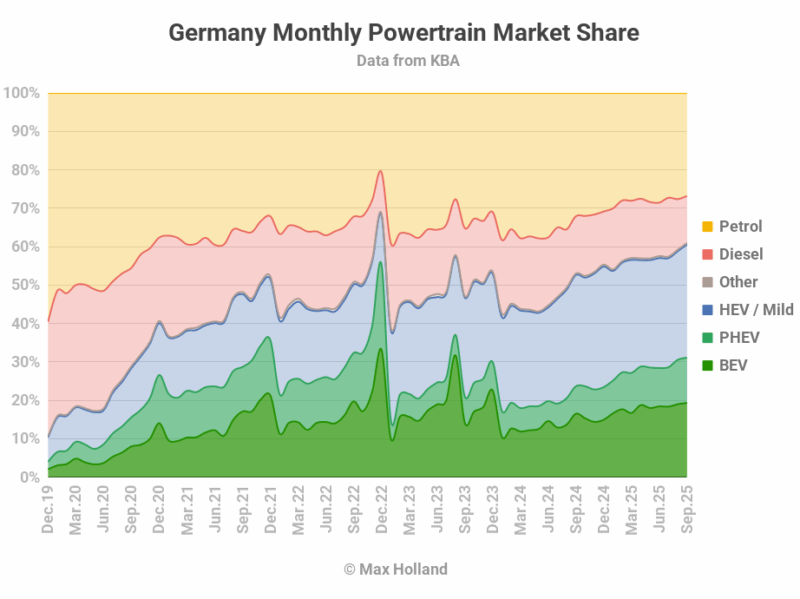

Since 2024 was a low baseline, let’s have a look at the YTD progress vs. each 2024 and 2023. Mixed plugins at the moment are at 28.4% YTD, with 18.2% BEV and 10.3% PHEV. 2024’s respective figures had been 19.3%, with 13.1% BEV and 6.3% PHEV. 2023’s respective figures had been 23.9% with 18.1% BEV and 5.8% PHEV.

So though 2025 is wanting a lot better than 2024, with a 9.1% extra share of the market going to plugins, it is just marginally higher than the identical interval in 2023. All of that marginal enchancment is all the way down to the expansion of PHEVs over the 2 intervening years.

What’s additionally completely different since 2023 is the dearth of BEV incentives now (after being cancelled in December of that 12 months). Briefly, the transition has recovered from that trauma and is now advancing below its personal steam (a extra strong path than counting on incentives) – and is much less weak to future setbacks.

PHEVs are again to a share they final noticed in 2021 and 2022, however the distinction this time round is that the brand new era of PHEVs have an electrical vary of over 80 km generally (vs. largely below 50 km beforehand). This era is thus extra more likely to contribute to “largely electrical km” of the general car fleet throughout their 15+ 12 months lifespan. As Germany’s transition continues over the subsequent couple of years, PHEVs will plateau after which fade away, as they did in Norway.

Combustion-only powertrains proceed to decrease (additional aided by HEVs grabbing 1.8% extra share of the market YoY). Their mixed YTD share is now all the way down to 42.6% (14.6% diesel and 28.0% petrol). This compares with 54.4% a 12 months in the past (17.9% diesel and 36.4% petrol).

We could count on December 2025 to see mixed ICE-only share to achieve near 35% for the month, and below 40% for the total 12 months.

Finest-Promoting BEV Fashions

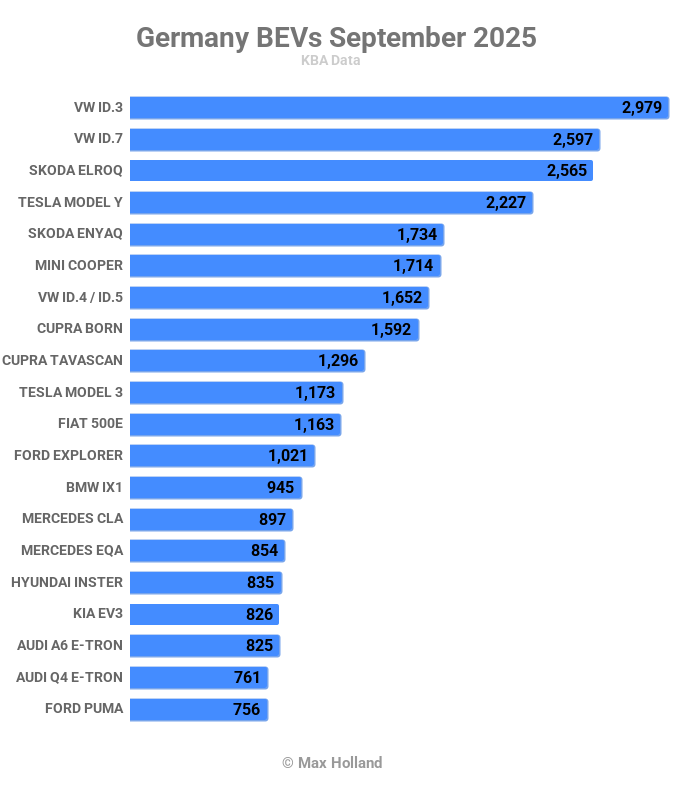

Having had a quieter first half of the 12 months, the Volkswagen ID.3 staged a comeback to take the pole-position in July, and has remained on the prime ever since – a formidable feat – with 2,979 items in September.

The ID.3’s sibling, the Volkswagen ID.7 – which had been dominating in H1 – took second place in September, with 2,497 items. Their cousin the Skoda Elroq took third place, with 2,565 items.

For me, the Skoda Elroq continues to face out as the good success story of the 12 months by way of its fast ascent to recognition. Having solely debuted in February, it was within the prime 10 by March, and the highest 5 by April. It has largely been within the prime 3 since Could, an incredible consequence. It’s additionally various car given the beginning value of €33,900 – a price proposition which has been key to its success.

Simply outdoors the September podium, in fourth, the Tesla Mannequin Y recovered a little bit of floor in its end-of-quarter push, however not again to the degrees of its outlandish dominance over the previous three years. As a reminder, the Mannequin Y was Germany’s best-selling BEV in 2022, 2023, and in 2024. Yr-to-date 2025, nevertheless, it solely ranks ninth! It might make up one or two locations in a giant December push, however this can be a putting fall-from-grace within the nation which produces all of Europe’s Mannequin Ys (on the Berlin-Brandenburg Gigafactory).

Aside from the standard month-to-month variations in rating, there have been two vital new entrants to the highest 20 in September. The brand new Mercedes CLA sedan, which solely noticed its first first rate buyer volumes in July, has now stepped as much as 14th spot, with 879 items.

Maybe much more importantly, for the mass-market transition, the brand new Ford Puma additionally noticed its entry into the highest 20 for the primary time since debuting in April. It grabbed twentieth spot with 756 items in September. As a reminder, the Puma begins from €36,900, and will have room to trim these costs if and when Ford will get critical.

There have been two correct debutants in September, and a pair extra fashions seeing pre-sale testing items. Kia launched their EV4, with 228 preliminary items, a powerful begin. The EV4 is a C-segment hatchback, with a size of 4,430 mm, styled like a shrunken model of its older sibling, the EV6 (4,680 mm). It begins from €37,900 for the 55 kWh (usable) variant, with 406 km WLTP, and 10-80% charging in half-hour.

Leapmotor launched the B10 SUV, a bigger C section providing, with a size of 4,515 mm. This one begins from a really aggressive €29,900 for the bottom 55 kWh (usable) LFP battery, with 361 km (WLTP), and 10-80% charging in 24 minutes. A 65 kWh (usable) possibility (434 km WLTP) is on the market from €32,400. The Leapmotor B10 is a superb worth proposition, let’s see the way it will get on in Germany.

Suzuki registered 6 items of their new Suzuki e-Vitara (see right here for specs), nevertheless it’s not but orderable on their web site, so we must wait longer for buyer deliveries. Likewise, the Changan sub-brand, Deepal, registered some testing items of its S05 and S07 fashions, however these are not but out there to order on the web site. We’ll revisit these when correct buyer volumes arrive. Kia additionally registered a single unit of their new PV5 modular van, however once more, that is for testing-only for now.

As for the small-and-affordable segments, within the sub-€20,000 vary, the Leapmotor T03 bought a formidable 630 items, and the Dacia Spring bought 359 items. Transferring as much as the €20-25,000 value vary, the chief right here was the Hyundai Inster, with 835 items, adopted by the Citroen e-C3 with 388 items, and the BYD Dolphin Surf, with 344 items. The Fiat Grande Panda scored 140 items.

Within the €25-29,999 value section, the Volkswagen ID.3 is priced inside this vary within the home market (not like in most different European markets, e.g. it’s €34,990 in France). So clearly the ID.3 dominates quantity right here, with its 2,979 items. Likewise, the Mini Cooper now comes inside this threshold in Germany (however is far more costly in most neighbouring markets), and bought 1,714 items. The (a lot weaker) first era Mini Cooper BEV was priced from €32,500 in Germany, so its value (and worth) has improved significantly. The Opel Corsa noticed 676 items, the Renault 5 bought 457 items, the Opel Frontera, 269 items, and the Renault 4 noticed 159 items. The Leapmotor B10 additionally begins inside this threshold, so let’s keep watch over it within the months forward.

In sum, 8,972 BEVs with beginning costs under €30,000 had been registered in September, some 20% of Germany’s complete BEV market.

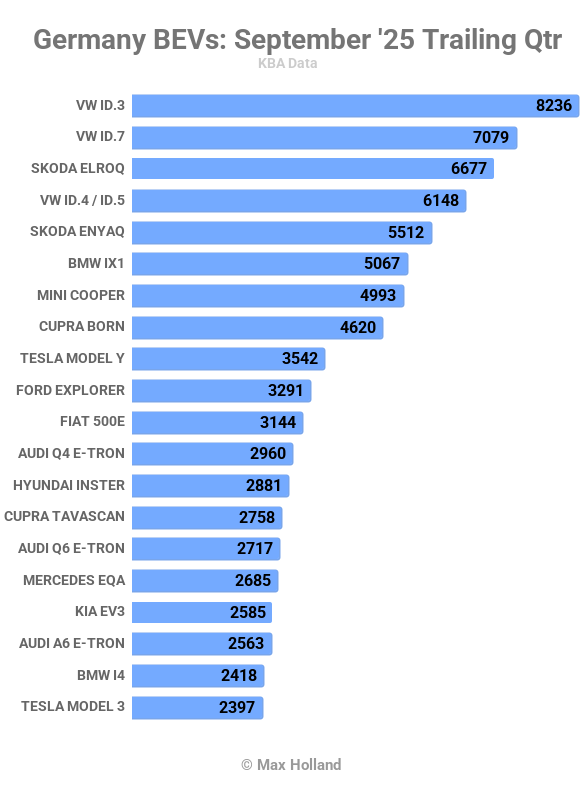

Let’s now examine the trailing 3-month rankings:

Given what I discussed above concerning the VW ID.3’s latest string of pole-positions, clearly it leads the Q3 chart, with a wholesome hole over its sibling the ID.7. The Skoda Elroq is in third.

Many of the higher ranks are fairly secure, and there have been no first time entrants to the highest 20. Simply outdoors, the Renault 5 climbed 3 spots for the reason that prior interval, to twenty second place, and will enter the highest 20 earlier than the top of the 12 months. The Leapmotor T03 has simply had its largest three months, and now stands in twenty eighth place (from thirty ninth prior).

The brand new Mercedes CLA has already climbed to twenty ninth place, and we’d count on it to creep into the desk by December. Likewise the brand new Ford Puma has now climbed to thirty third and nonetheless has room to develop.

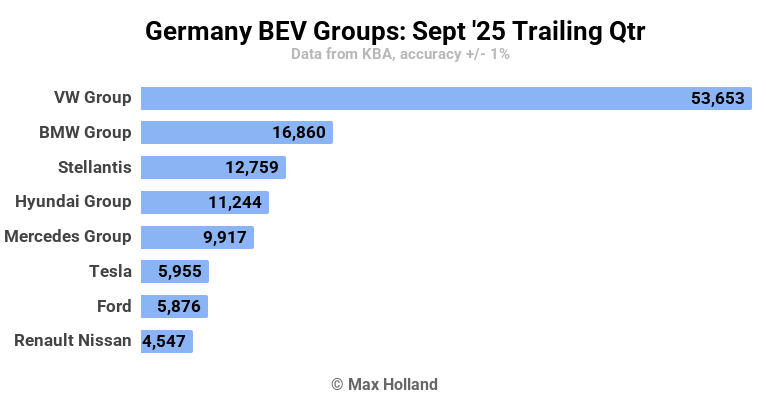

Let’s now have a fast examine on the manufacturing teams:

The highest 5 rankings stay unchanged. Volkswagen Group stays dominant, although share has dropped from Q2’s 45.6% all the way down to 40.8%.

BMW Group’s share elevated from 11.5% to 12.8%. Stellantis elevated from 8.8% to 9.7%. HMG was barely modified, and Mercedes Group elevated from 6.1% to 7.5%.

Tesla recovered a bit, climbing from eighth to sixth and from 2.9% to 4.5% however seemingly received’t overtake Mercedes Group between now and December.

Outlook

Germany’s total year-to-date auto market is roughly unchanged in quantity from 2024. PHEVs have been the primary development story in 2025, on the expense of combustion-only powertrains.

The German financial system stays stagnant, with the newest GDP knowledge from Q2 2025 displaying weak YoY development of 0.2%. Inflation crept as much as 2.4% in September from 2.2% in August. ECB rates of interest have been flat at 2.15% since early June. Manufacturing PMI fell to 49.5 factors in September, from 49.8 factors in August.

What are your ideas on Germany’s progress? The place will BEV share be in December, and over full-year 2025? Please share your insights and views within the feedback under.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our every day publication, and comply with us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day publication for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if every day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage