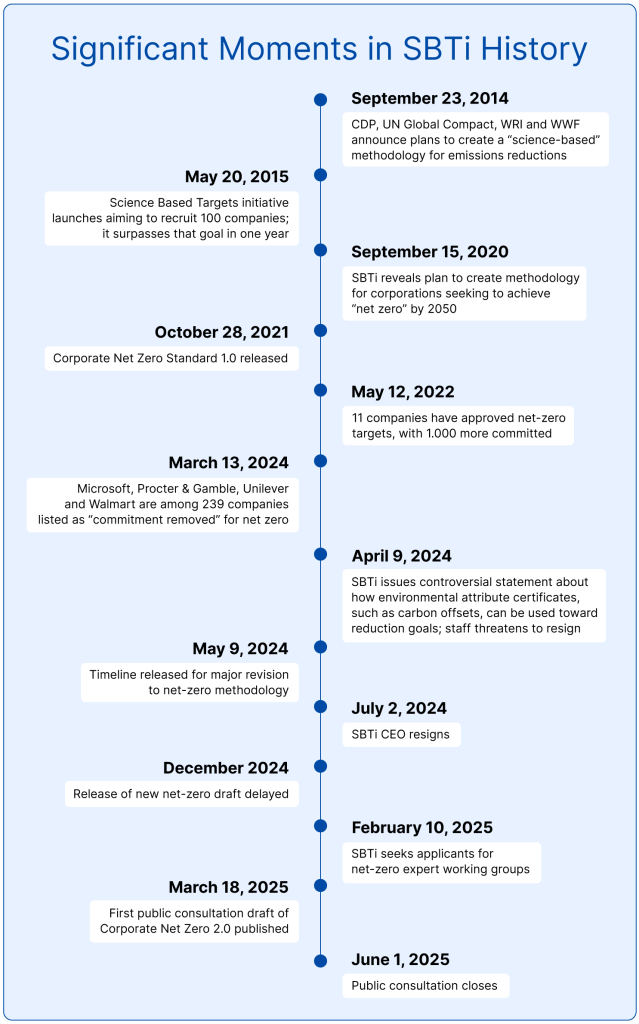

The Science Primarily based Targets initiative has printed a 132-page “preliminary session” doc describing proposed revisions to the Company Web Zero Customary.

SBTi’s methodology has develop into the de facto framework that guides corporations in setting science-based targets for emissions reductions that search to carry international temperature will increase under 1.5 levels Celsius by 2050.

The draft has been delayed for months amid arguments over SBTi’s course and a CEO resignation. Greater than 3,000 corporations have introduced plans to decide to web zero. About half have really had their targets validated, and about one-third are small or midsize corporations.

Nothing in the proposal printed March 18 is technically remaining. SBTi has assembled 5 skilled working teams to critique the revisions. Additionally it is soliciting suggestions by way of a web-based survey till June 1. From there, revisions might be made, and a brand new draft might be circulated for one more spherical of feedback earlier than SBTi’s technical crew and board contemplate them for approval.

Sweeping adjustments to Scope 3 methodologies

Some adjustments proposed within the draft might be more durable for corporations to satisfy than the present net-zero normal, however SBTi is extra versatile about necessities some companies have criticized — particularly its methodology for Scope 3 emissions from company provide chains.

Greater than half the businesses surveyed by SBTi pointed to dealing with Scope 3 as their most vital problem when aiming to develop into web zero. Revisions proposed within the draft would dramatically change that course of. Key examples:

- Scope 3 targets are necessary for large corporations (these with greater than $450 million in income), whatever the proportion they contribute to general emissions.

- Corporations might want to establish their most emissions-intensive actions — sources that account for at the least 1 p.c of Scope 3 or that generate greater than 10,000 metric tons of carbon dioxide tools per yr.

- SBTi proposes dropping the fastened percentages it beforehand utilized for setting Scope 3 targets in favor of a system that might permit corporations to focus as an alternative on “related” classes — people who account for at the least 5 p.c of their Scope 3 footprint.

- Corporations should use “direct affect” to require tier one suppliers (these with which it has a direct relationship) to set their very own net-zero targets.

- Targets can take completely different varieties — starting from absolute emissions reductions to proof of “net-zero-aligned” procurement actions, similar to shopping for metal or cement from suppliers which are lowering their manufacturing emissions in keeping with a plan to succeed in web zero.

- SBTi is extra open to the thought of “oblique mitigation” of actions that corporations can’t immediately management. That may imply, for instance, shopping for sustainable aviation gasoline certificates via a book-and-claim system to cut back emissions associated to air journey. It may additionally imply setting different procurement targets for decrease carbon variations of supplies that usually have excessive emissions, similar to metal or concrete.

Into account: Suggestions for carbon removing targets

The trail to web zero has at all times acknowledged the necessity to let corporations abate residual emissions on the finish of their journey; often lower than 10 p.c of the carbon footprint for his or her baseline yr.

The draft contains options that might let corporations get credit score for “high-integrity” carbon removing actions going down between now and their net-zero goal yr (often 2050).

Listed below are three pathways being thought of as a part of the brand new session:

- Possibility 1: Require corporations to set carbon removing and abatement targets for the close to time period and long run aimed toward mitigating projected residual emissions of their net-zero yr.

- Possibility 2: Acknowledge corporations that set near-term and long-term carbon removing and abatement targets for that function.

- Possibility 3: Give corporations flexibility for the way they deal with residual emissions.

The choices above pertain particularly to residual emissions that an organization isn’t in a position to abate by its net-zero yr. SBTi can be exploring whether or not to “acknowledge” corporations for utilizing carbon credit and different mechanisms to handle the annual emissions generated as corporations transition to web zero, which it refers to as “ongoing” emissions. However the draft doesn’t go into element about what kind the popularity would take.

Stricter governance expectations and different notable adjustments

The replace proposes completely different standards for big and small corporations; there are additionally nuances associated to geography. And all that is simply the tip of the iceberg. Corporations can even must:

- Set net-zero objectives extra shortly. As soon as massive corporations decide to setting targets, they’ll have one yr to ship as an alternative of the 2 years they beforehand needed to get validated. Smaller corporations nonetheless get two years.

- Anticipate spot checks. The draft suggests “any firm and goal” is topic to random assessments to substantiate conformity with the usual and guarantee integrity. Potential triggers for that type of scrutiny embrace a reputable grievance.

- Brace for normal baseline information evaluations. SBTi needs corporations to reevaluate their base yr emissions on an annual foundation and every time there’s a giant group change, similar to a merger or divestment.

- Write a local weather transition plan. The draft recommends publishing one inside 12 months of getting a net-zero goal validated. These are disclosures that describe investments and enterprise mannequin adjustments a company should make to carry international temperature will increase to 1.5 levels Celsius. Roughly one in 4 corporations that make voluntary annual disclosures to researcher CDP do that.

- Hold shut scrutiny on baseline years. The group needs them to be “consultant of precise construction and efficiency.” Beforehand, it allowed corporations to succeed in way back to 2015. The revision would require corporations to pitch a baseline no sooner than three years earlier than their preliminary validation. Plus, massive corporations will want a 3rd get together to guarantee their emissions stock calculations.

- Shift to higher information assortment processes. SBTi is pushing for corporations to display extra use of major information, and for steady enhancements in how they hint emissions from suppliers. Full traceability for his or her most emissions-intensive actions is predicted by 2035.

- Renewals may very well be required extra shortly. Targets are usually set in five-year cycles. After that interval, corporations must set new ones. Sure occasions may power an earlier renewal, such because the divestment of a enterprise line or the necessity for a baseline yr emissions recalculation.

Window for public session open

The group will contemplate enter on the entire revisions within the Company Web Zero 2.0 draft between March 18 and June 1.

Over the summer season, SBTi will evaluate the suggestions to find out the place changes or clarifications are wanted; it plans to publish a abstract of that enter and the way it’s being addressed, however no particular timeline for that course of has been disclosed.

Adjustments might be included into a brand new draft that might be circulated for a second public session, earlier than it’s in the end submitted for approval by the SBTi technical council. The ultimate step for adoption is a vote by the SBTi board of trustees.

“That is an iterative course of and the general public session will assist us establish the adjustments we will make to make sure SBTi’s revised normal creates affect at scale as successfully as doable,” stated Alberto Carillo Pineda, chief know-how officer at SBTi.

For 2025 and 2026, corporations can nonetheless set science-based emissions discount targets for 2030 utilizing the present Company Web Zero and Close to-Time period Standards methodologies. Targets set in these years might be legitimate for both 5 years or till the top of 2030, whichever is earlier.

Beginning in 2027, SBTi expects corporations to set targets in keeping with the finalized model of Company Web Zero Customary 2.0, due by the top of 2026.

Are you a company sustainability skilled who’d like to debate the proposed updates? Join with me on LinkedIn (or e mail me) to start out a dialogue.