Over the previous three years, battery recycling has obtained heightened consideration, elevating vital questions: What’s the true state of recycling at the moment? Can it present the U.S. and EU with safe entry to vital minerals, or is recycling a waste of assets given their lack of refining capability?

The fact is that recycling alone won’t present ample productive quantity to satisfy total demand. Nonetheless, recycling has the potential to play an essential function in making a extra round and sustainable financial mannequin, particularly as applied sciences refine their market match.

The Financial Realities Of Recycling Form The Broader Panorama Of Steel Recycling?

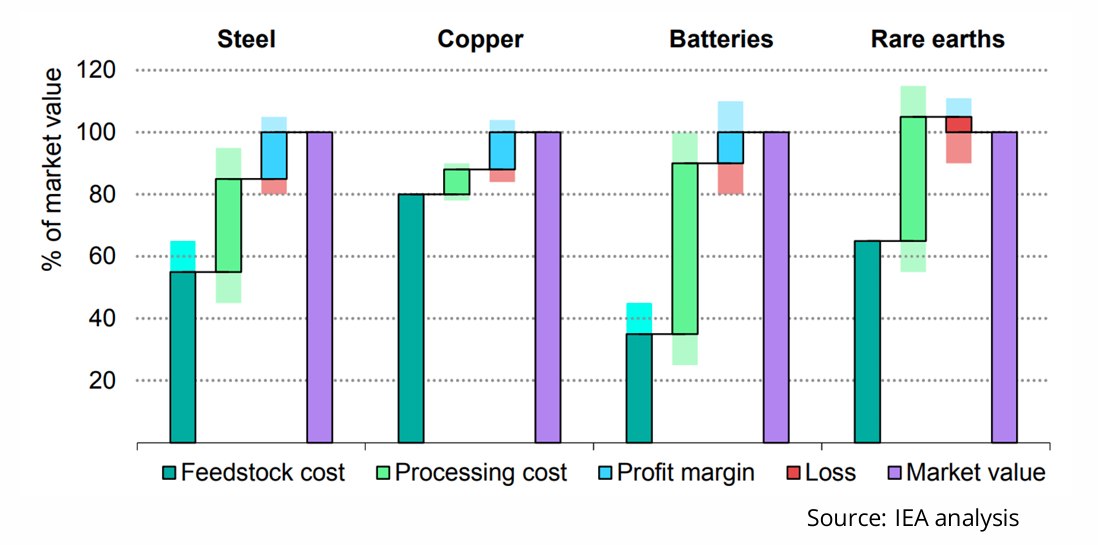

Recycling economics fluctuate throughout metal, copper, batteries, and uncommon earths. Metal and copper profit from mature infrastructure and steady pricing, whereas batteries and uncommon earths face excessive prices and fragmented know-how stacks. Battery recycling earnings are additionally unstable resulting from shifting lithium and cobalt costs, international refining bottlenecks, and transport points. Whereas this primarily applies to NMC (nickel manganese cobalt), LFP (lithium iron phosphate) chemistries, variants additionally present notable, although totally different, volatility.

Financial Evaluation of Materials Recycling

With China dominating refining, uncommon earth recycling faces tight provide chains. In contrast to batteries, it’s not but worthwhile and is principally pushed by strategic worth.

Though the EU not too long ago started shifting funding towards uncommon earth initiatives, battery recycling start-ups have nonetheless struggled to achieve lasting traction, as mirrored in Glencore buying Li-Cycle and Lyten shopping for out Northvolt. The important thing query now: which corporations will stand out, and can or not it’s by way of know-how innovation, price management, or strategic provide chain positioning?

Regional Aggressive Fashions

Financial realities of battery recycling fluctuate considerably by area, pushed by China’s management of over 80% of key materials refining. This dominance has profound implications for the sector’s economics and aggressive panorama.

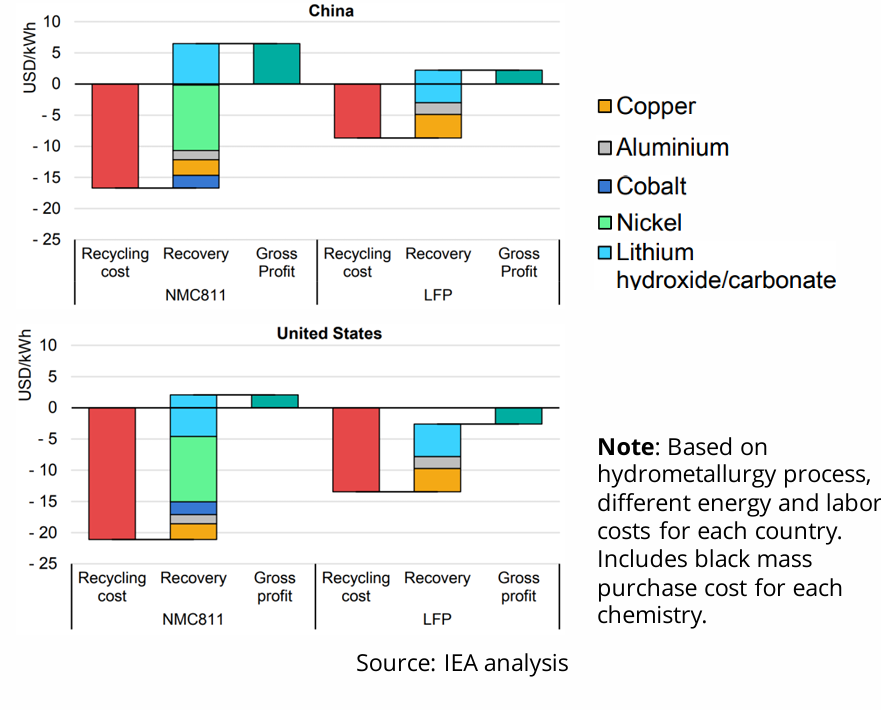

Battery Recycling Economics within the U.S. and China

Recycling NMC batteries within the U.S. is barely worthwhile, whereas LFP and different sorts aren’t economical. In China, each NMC and LFP may be recycled profitably because of industrial scale, vertical integration, and decrease working prices.

Three elements set China other than North America and Europe:

- Battery Chemistry – China can recycle a number of battery sorts, NMC, LFP, and others, collectively at scale, owing to its sturdy base in cell and cathode manufacturing

_ - Supplies Pricing – Nickel and cobalt make NMC interesting to U.S. recyclers, whereas China’s various supplies combine helps maintain recycling worthwhile throughout chemistries

_ - Location and Labor – China’s expert labor prices are sometimes half these within the U.S., and its recycling vegetation are 5 occasions bigger—boosting effectivity and scale

Different Regional Fashions

- Australia – Constructing a vertically-integrated lithium provide chain, together with recycling capabilities

_ - South Korea – Linking superior recycling to its sturdy manufacturing base

_ - India and Thailand – Focusing on low-speed EV markets by way of collaborations equivalent to Tata with Lohum, markets largely missed by China

Innovation in processing and disassembly shall be vital:

- Assortment & Sortation: Robotics and automation can enhance effectivity if chemistries are standardized and simply identifiable

_ - Disassembly: Automation reduces security dangers like fires and fluoride publicity

_ - Preprocessing: A bottleneck within the U.S. and EU, the place corporations equivalent to Cyclic Supplies (automation) and Blue Whale Supplies (transport price discount) are rising as key gamers

LIB Recycling Innovator Panorama

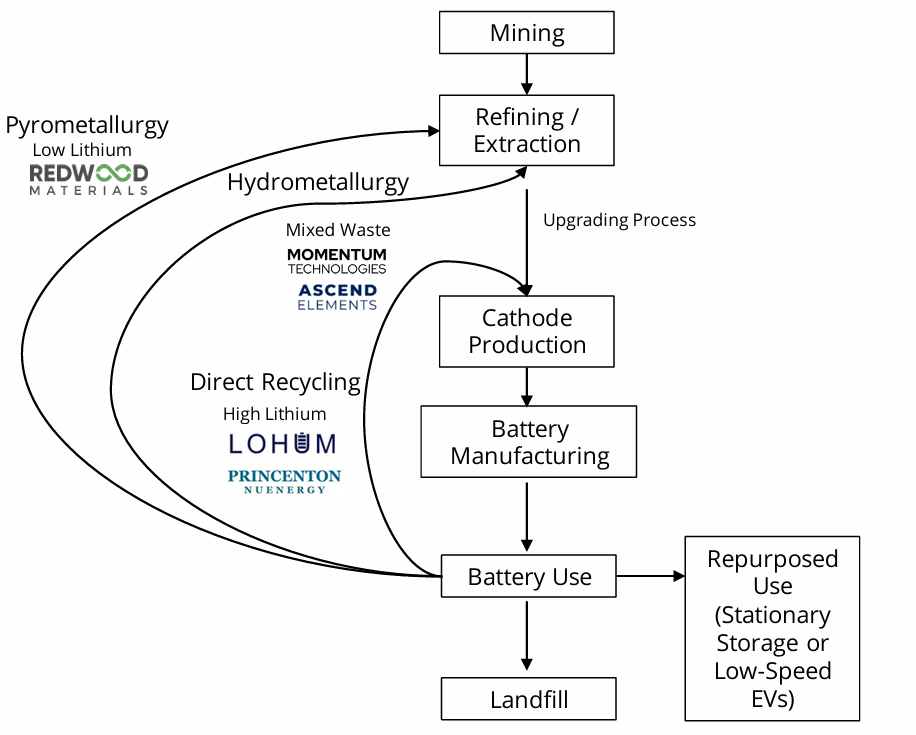

Technologically, hydrometallurgy and direct cathode recycling present probably the most promise, whereas pyrometallurgy is fading resulting from inefficiency and lithium losses.

Limitations of Pyrometallurgy

Pyrometallurgyfaces elementary limitations that constrain its long-term viability. Chief amongst these is its incapability to protect lithium. The method successfully destroys most lithium content material, making it unsustainable as demand for lithium intensifies. Decrease-temperature variants may be mixed with subsequent hydrometallurgical processing, however these hybrid approaches incur important vitality losses and effectivity trade-offs. From each an financial and technological perspective, this pathway is unlikely to stay aggressive.

Hydrometallurgy and Rising Innovators

Hydrometallurgy has emerged because the main recycling know-how in most superior markets. As a water-based course of, it excels at dealing with combined waste streams and is adaptable to various chemistries. New entrants are innovating inside this framework:

- Momentum Applied sciences is creating modular hydrometallurgical models deployed straight at preprocessing websites, aiming to scale back transportation prices and bypass middleman recyclers

- Ascend Parts: After preliminary success in North America, is now increasing into Europe. Its skill to scale whereas adapting to Europe’s extra advanced regulatory and market setting shall be a key check

Direct Recycling: A Strategic Shift

Direct cathode recycling is the sector’s most disruptive innovation—it retains the cathode’s crystalline construction intact and wishes much less reprocessing than hydrometallurgy and pyrometallurgy, making it perfect for areas with out large-scale refining however rising mineral demand. Because the market shifts towards LFP batteries, direct recycling turns into much more related. Corporations like Princeton NuEnergy and Lohum are scaling up with new applied sciences, providing a means for locations like Europe, South Korea, Japan, and the U.S. to bypass refining bottlenecks and feed recovered supplies straight again into manufacturing.

Coverage and Market Situations: Wanting Forward

World competitiveness in battery recycling shall be formed not solely by know-how, but in addition by coverage:

- Enterprise-as-Normal: China continues to consolidate its dominance in refining and recycling, with declining LFP costs reinforcing its place as the only economically viable market

_ - Area of interest Market: China retains management of the mainstream trade, whereas different areas preserve restricted, region-specific recycling operations constrained by restrictive or short-sighted insurance policies

_ - Market-Profitable: Strong coverage assist allows the event of built-in provide chains centered on direct recycling, permitting the U.S., EU, Korea, and Japan to determine aggressive industries regardless of larger operational prices.

Coverage Will Be the Decisive Issue

The EU’s initiatives present ambition however danger with out safe feedstock, whereas China’s easing of black mass restrictions signifies an rising try and consolidate battery recycling feedstock. To realize a aggressive place, governments should pair assist for direct recycling with improved preprocessing, feedstock entry, and integration into home manufacturing capabilities.